Marginal cost is defined as: the change in total costs from producing one more unit of output.

Discipline: Economics

Type of Paper: Question-Answer

Academic Level: Undergrad. (yrs 3-4)

Paper Format: APA

Question

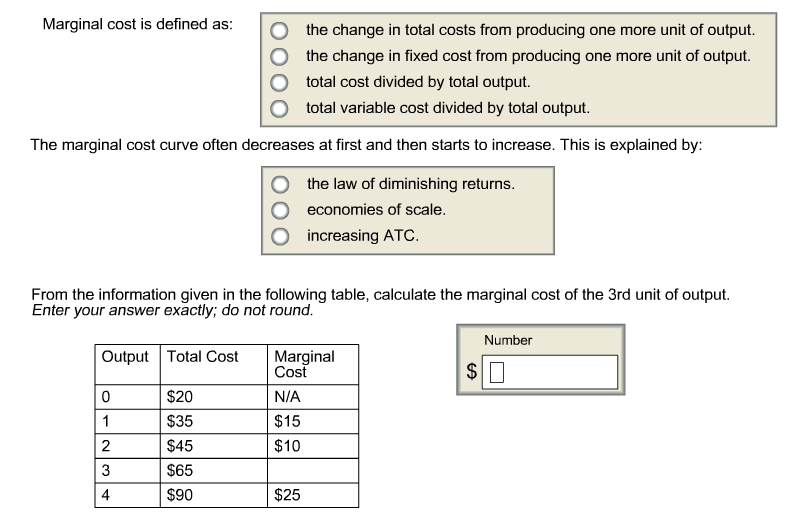

Marginal cost is defined as: the change in total costs from producing one more unit of output. the change in fixed cost from producing one more unit of output. total cost divided by total output. total variable cost divided by total output. The marginal cost curve often decreases at first and then starts to increase. This is explained by: the law of diminishing returns. economies of scale. increasing ATC. From the information given in the following table, calculate the marginal cost of the 3rd unit of output. Enter your answer exactly; do not round

Expert Answer

Answer A is correct.

Definition of Marginal cost is -: Marginal cost is the change in total cost from producing one more unit output.

Answer A is correct.

The marginal cost curve often decrease at first and then statrts to increase. this is explained by the law of diminishing returns.

Marginal cost for 3rd unit is $20. where n=3 TCn = 65 , TC(n-1) = 45

MCn = TCn - TC(n-1) , using this formula

= 65 - 45